Tarsadia Capital Sends Letter to Board of Sunstone Hotel Investors, Inc.

Calls on Sunstone Board to Immediately Commence a Process to Pursue a Sale of the Entire Company or Plan of Sale and Liquidation of the Company’s Assets

Sunstone is a Subscale and Undervalued REIT in an Underperforming Sector

Board Requires Urgent Refreshment, Must Appoint Shareholder Focused Directors to Lead the Value Maximization Process

NEW YORK, Sept. 12, 2025 (GLOBE NEWSWIRE) -- Tarsadia Capital, LLC including its affiliates and managed funds (“Tarsadia Capital”) a 3.4% economic interest holder of Sunstone Hotel Investors, Inc. (“Sunstone” or the “Company”) today, sent a letter to the board of directors of Sunstone (the “Board”) calling on the Company to immediately commence a two-track process to pursue a sale of the entire Company or a plan of sale and liquidation of the Company’s assets, to preserve and maximize value for shareholders.

“Sunstone’s current trajectory as a subscale lodging REIT is simply not tenable. The Board needs immediate refreshment and must commence a robust strategic alternatives process to unlock value for shareholders. As a long-term and engaged shareholder, Tarsadia Capital has encouraged the Board to act with urgency on the Company’s persistent undervaluation in the public markets, but to no avail. If the Board desires to continue with the status quo, we are prepared to make the case for change directly to our fellow shareholders,” said Michael Ching, Tarsadia Capital.

The full text of the letter follows:

September 12th, 2025

Board of Directors

Sunstone Hotel Investors Inc.

15 Enterprise, Suite 200

Aliso Viejo, CA 92656

Dear Members of the Board:

We are writing to you on behalf of Tarsadia Capital, LLC, together with certain of its affiliates and the funds it manages (“Tarsadia,” “our,” “us” or “we”), which beneficially owns a 3.4% economic interest in Sunstone Hotel Investors, Inc. (“Sunstone” or the “Company”), making us the second largest active shareholder of Sunstone, just behind Blackstone, Inc. We are the public investment management arm of a family office that has significant expertise owning, operating and investing in the lodging and hospitality sector.

Tarsadia has a deep history with Sunstone, having (i) sold hotels to Sunstone prior to its IPO in 2004, (ii) been public investors in its stock, (iii) visited all 14 of its properties, and (iv) interacted regularly with the executive management team.

However, we believe Sunstone’s portfolio of 14 hotel properties, down from 60 properties in 2005, is subscale and undervalued by public market investors. These factors—and the significant negative sentiment pressuring the Lodging REIT sector—have led to the persistent poor performance of the Company’s stock.

As we have articulated to the board and management team, the Company’s current trajectory is not tenable, and in order to preserve and maximize value for shareholders, Sunstone must immediately commence a two-track process to market its properties and/or pursue a sale of the entire Company.

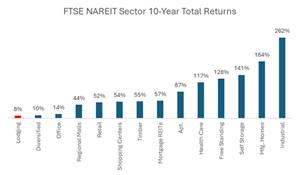

The Lodging Real Estate Investment Trust (“REIT”) Industry

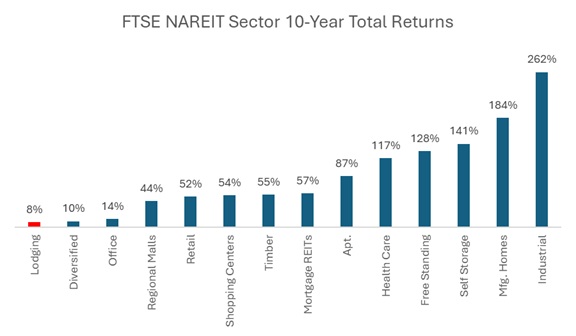

Sunstone and its Lodging REIT peers have achieved the worst 10-year total return among all FTSE Nareit US Real Estate Property Sectors.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/d4455217-8a08-405b-8d0c-cda2bb5be7f5

Source: Bloomberg. 10-year returns through September 9, 2025.

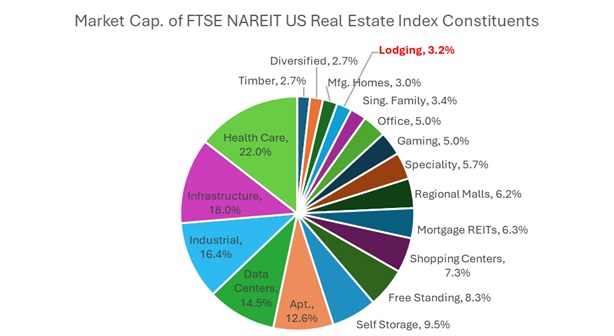

This sector-wide share price underperformance has led to Lodging sector equity market capitalization representation in the FTSE Nareit US Real Estate Index declining from 4.5% in 2013 to 3.2% at the end of July 2025, becoming the 4th smallest REIT sector, just above niche markets: Timber (2.7%), Manufactured Homes (3.0%) and the catch-all, “Diversified” (2.7%).

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/06589b24-cc9e-445a-910b-1c937e1f2710

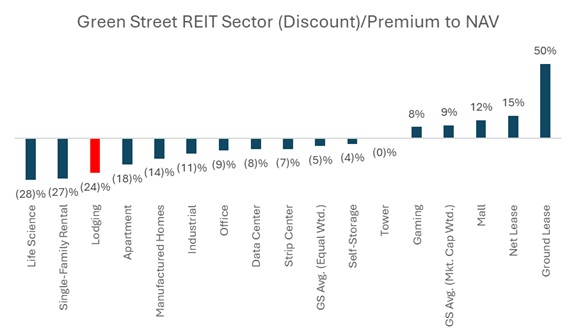

The Lodging REIT sector also trades at one of the steepest discounts to its net-asset-value (“NAV”) among its peers, reflecting its lack of acceptance by public equity investors.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/ab5a7a00-2412-41c8-a10a-134e251bf083

Source: Green Street research as of September 2, 2025.

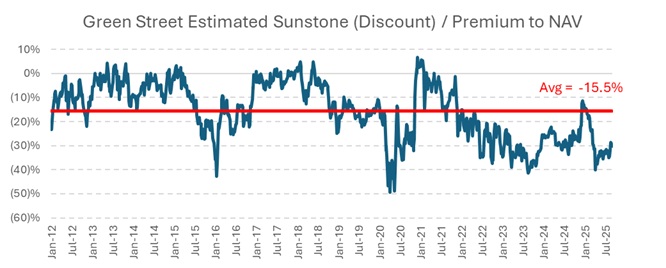

Sunstone’s estimated discount to NAV of -30% as of September 2, 2025 is near the Company's 13-year lows, and well below its long-term average of -15.5%.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/678891ca-b915-4a29-8d4e-9caa2a3aa7b6

Source: Green Street research as of September 2, 2025.

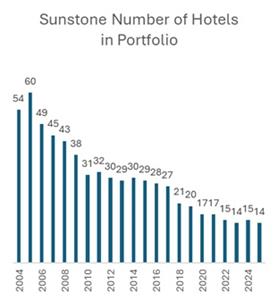

Sunstone Today

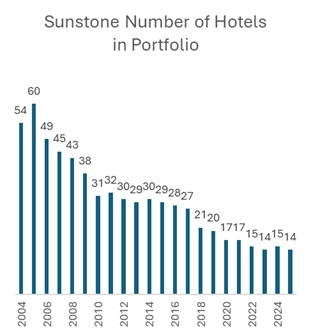

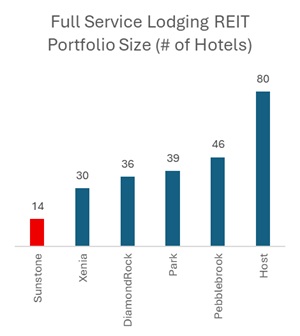

Sunstone has contributed to the Lodging REIT sector’s shrinking relevancy and abysmal returns. As discussed above, the Company reached a peak of overseeing 60 hotels in its portfolio in 2005, but that has now shrunk down to 14 hotels, the smallest of its full-service Lodging REIT peers. Wall street sell-side analysts have also taken note of Sunstone’s shrinking portfolio, which has led analysts to question the Company's viability. For instance, at the Company's August 6, 2025 earnings call, Wells Fargo analyst Jack Armstrong alluded to this pressing problem when he asked management point blank, “In your view, at what point does the size of the [C]ompany become a hurdle for potential investors?”

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/ae0322a8-4c69-4bd5-b25b-416dfb90a3f3

Source: Company filings.

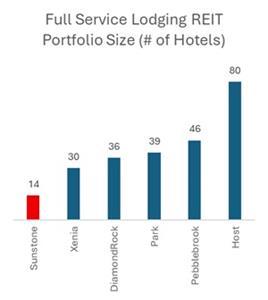

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/4aacdc4d-0201-4655-af79-28bbd68a3bee

Source: Company filings, as of June 2025.

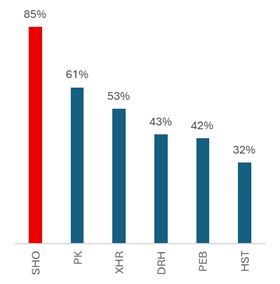

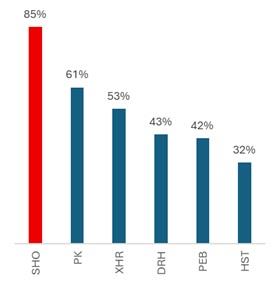

Sunstone’s small portfolio leads to concentration issues, where a single weather event, market catalyst or renovation can substantially change the earnings profile of the Company. Currently, Sunstone’s top seven properties represent 85% of its total EBITDA, with the Hilton San Diego Bayfront—its largest hotel—contributing to 19% of its total EBITDA. Meanwhile, the Company's peer full-service Lodging REITs have much more diversified portfolios where the top seven properties represent 32% to 61% of EBITDA.

Sunstone Property EBITDA Concentration

| Property | % of EBITDA |

% Cum. EBITDA |

|

| Hilton San Diego | 19% | 19% | |

| Wailea Marriott | 18% | 37% | |

| Westin Washington DC | 12% | 49% | |

| Marriott Boston | 10% | 59% | |

| Renaissance Orlando | 10% | 69% | |

| Hyatt San Antonio | 8% | 78% | |

| JW Marriott New Orleans | 8% | 85% | |

| Montage Healdsburg | 4% | 89% | |

| Hyatt San Francisco | 4% | 93% | |

| Oceans Edge | 3% | 97% | |

| Marriott Long Beach | 3% | 99% | |

| Four Seasons Napa | 1% | 101% | |

| Marriott Portland | 1% | 102% | |

| Andaz Miami | -2% | 100% | |

Source: Company filings, as of June 2025.

Lodging REIT EBITDA % of Top 7 Properties

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/f40594c2-0314-4da5-ac26-b516357257eb

Source: Company filings, as of June 2025, except for HST, which is as of December 2024.

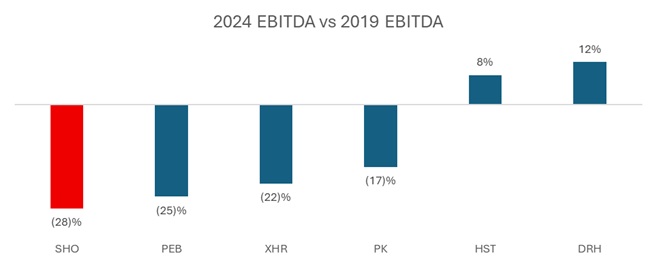

Sunstone’s financial performance has also suffered, with 2024 EBITDA -28% below 2019 levels, the lowest among its full-service lodging REIT peers.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/3953fd9b-1830-4847-bcd2-1d0fca7103ea

Source: Company filings.

The Time for Change is Now

Many publicly traded REITs have been frustrated with their share price underperformance and trading levels at significant discounts to NAV. However, several public REIT boards have determined to take proactive steps to preserve and maximize value for shareholders. For example, on August 4, 2025 the Board of Elme Communities, a multi-family REIT, announced the conclusion of its strategic alternatives review process. Elme Communities decided to sell a substantial portion of their assets, liquidate the remaining assets and return all capital to shareholders.

Then, on August 26, 2025, lodging REIT Braemar Hotels & Resorts, Inc., announced that it is initiating a process for the sale of the company. Monty J. Bennett, Chairman of the Board of Braemar Hotels & Resorts noted in the press release, “the reality is that the public markets have not been friendly to lodging REITs, including Braemar.” Richard Stockton, CEO of Braemar Hotels & Resorts also noted, “With improving economic conditions, continued strength in industry performance, limited new room supply, and healthy consumer spending, I believe we are entering a favorable environment for a potential sale."

The Path Forward

In our discussion with management in August 2025, and certain board members in September 2025, we highlighted the need for Sunstone to take two vital actions:

-

Form a Strategic Review Committee to explore all value-maximizing alternatives, including a dual-track process to sell each of its 14 hotel properties and/or a sale of the entire Company. The Strategic Review Committee should be aided or led by (a) highly-qualified financial advisors and brokers and (b) a new independent director.

-

Refresh the Board by appointing new independent directors in mutual agreement with Tarsadia.

Conclusion

Sunstone has been a public company for over 20 years and has been on a journey of shrinking into obsolescence. To maximize value for shareholders, it is essential that this Board recognizes it is now time to realize the value of Sunstone’s portfolio before further value is destroyed. While it is disappointing to hear that the Board disagrees with our view on the urgency to act now, it is not surprising based on Sunstone’s financial and stock performance track record.

If the Board desires to continue with the status quo, we are prepared to make the case for change directly to our fellow shareholders.

Sincerely,

Tarsadia Capital

About Tarsadia Capital, LLC

Tarsadia Capital, LLC is the New York-based investment management company of a family office. Tarsadia Capital has a flexible and long-duration investment mandate that focuses on equities and commodities globally. Our investment process employs deep fundamental research on secular inflections to identify and build conviction around asymmetric risk/reward opportunities that will play out over multi-year time horizons.

Media Contact

Gagnier Communications LLC

Dan Gagnier & Riyaz Lalani

646-569-5897

Tarsadia@gagnierfc.com

Disclaimer

All statements contained herein that are not clearly historical in nature or that necessarily depend on future events are “forward-looking statements,” which are not guarantees of future performance or results, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” and similar expressions are generally intended to identify forward-looking statements. The projected results and statements contained herein that are not historical facts are based on current expectations, speak only as of the date of this letter and involve risks that may cause the actual results to be materially different. Certain information included in this material is based on data obtained from sources considered to be reliable. No representation is made with respect to the accuracy or completeness of such data. All figures are unaudited estimates and subject to revision without notice. Tarsadia Capital disclaims any obligation to update the information herein and reserves the right to change any of its opinions expressed herein at any time as it deems appropriate and without notice.

FTSE NAREIT Sector 10-Year Total Returns

FTSE NAREIT Sector 10-Year Total Returns

Market Cap. of FTSE NAREIT US Real Estate Index Constituents

Market Cap. of FTSE NAREIT US Real Estate Index Constituents

Green Street REIT Sector (Discount)/Premium to NAV

Green Street REIT Sector (Discount)/Premium to NAV

Green Street Estimated Sunstone (Discount) / Premium to NAV

Green Street Estimated Sunstone (Discount) / Premium to NAV

Sunstone Number of Hotels in Portfolio

Sunstone Number of Hotels in Portfolio

Full Service Lodging REIT Portfolio Size (# of Hotels)

Full Service Lodging REIT Portfolio Size (# of Hotels)

Lodging REIT EBITDA % of Top 7 Properties

Lodging REIT EBITDA % of Top 7 Properties

2024 EBITDA vs 2019 EBITDA

2024 EBITDA vs 2019 EBITDA

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.